On Monday, March 6th, Linden Lab announced a series of fee changes / payment changes to Second Life which have sparked some debate.

The announcement leads with the reduction in “standard” Full private region (i.e. a region with the standard 20,000 Land Capacity) monthly tier being reduced by US $20 a month, from $229 / month to US $209 / month – the reduction being to mark 2023 being SL’s 20th anniversary.

Note that the monthly Homestead tier and the US $30 / month for the Full Private region land capacity bonus remain unchanged.

It also introduces an option that has been requested numerous times over the years: the ability to pay tier on regions obtained directly from the Lab using Linden Dollars. However this option comes with some caveats:

It is limited to only one region per Premium Plus subscriber.

It is only available for Premium Plus subscribers.

It is currently a “beta” programme, currently set to end on September 6th, 2023 – although this date may change / be extended.

Land tier rates for regions in Linden Dollars – available for Premium Plus subscribers with land holdings, per the notes above. Table via Linden Lab.

Payments are made on the basis of a stable conversion rate of L$250 to the US dollar, and to facilitate payments, Linden Lab has created a Land Payments region, although at the time this blog post was written, it did not appear to be available. For further details on it, and the all information on using Linden Dollar to pay tier to Linden Lab, please refer to L$ Payments for Land.

Fee Changes

In what is likely to be a less popular move, the blog post notes the following Lindex fee changes, which come into immediate effect from Monday, March 6th, 2023:

The buy fee is increased to 10%, with the minimum and maximum fees charged remaining unchanged at US $1.49 and US $14.99 per transaction respectively.

The sell fee is increased to 5%, regardless of the size of the transaction.

The blog post notes that these increases are to offset the above land price reductions (and thus a continuation of LL’s policy of redistributing their means of revenue generation to be less reliant on a single product (land)), and also as a result of rising operational costs.

A brief FAQ on these changes is provided in the official blog post, and specific questions on them can be made through the forum thread associated with the blog post, or possibly submitted as a question which might be asked of the SL management team as a part of the Lab Gab session to be broadcast on Friday, March 10th (in which case the question must be submitted by 09:00 SLT on Thursday, March 9th, 2023.

The last few months of 2020 saw Tyche Shepherd release some brief summaries related to Second Life that – as always – make for interesting reading for those interested in the general state of the platform.

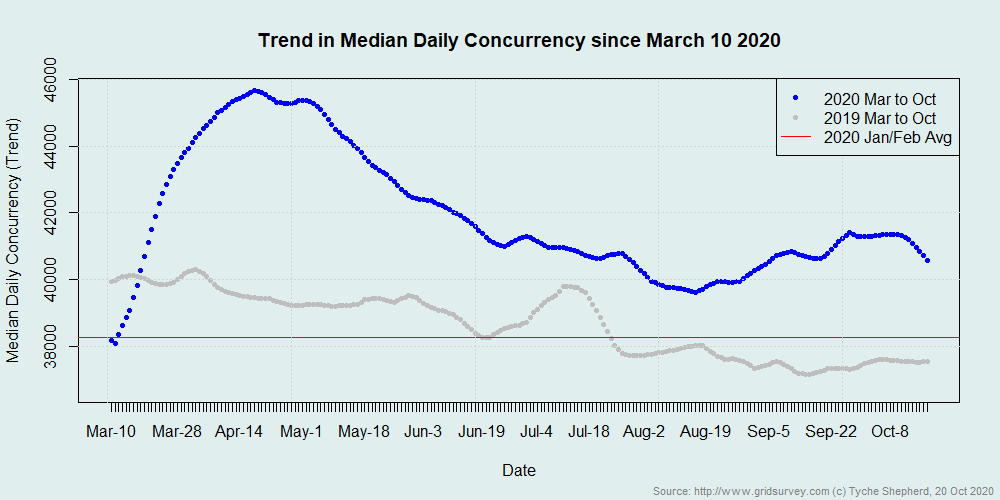

In the first, a tweet Tyche issued in October, we were offered insight into general use of the platform in terms of sign-up and concurrency. It came as a the last in a brief series of tweets from Tyche on the subject that started after the Lab indicated that with the spread of the SARS-CoV-2 pandemic, they were seeing an increase in general usage of the platform, particularly among returning users.

Following-on from Tweets in June -, Tyche confirmed that overall, median concurrency on the platform saw clear growth in March through mid-May (when the first ’bout of lockdowns hit a fair portion of the world due to the pandemic, before gradually falling through until mid-August, when a further “bump” occurred that lasted through until October (when Tyche made her Tweet). She also showed that overall, median concurrency remained well above that seen in 2019.

That concurrency is up can be taken as a good sign; it means that more people are engaging in the platform at any given period, allowing greater opportunities for interactions – which can be particularly important for incoming new users looking for things to do and people to meet. However, it is with regards to the latter that Tyche’s observations have been more mixed.

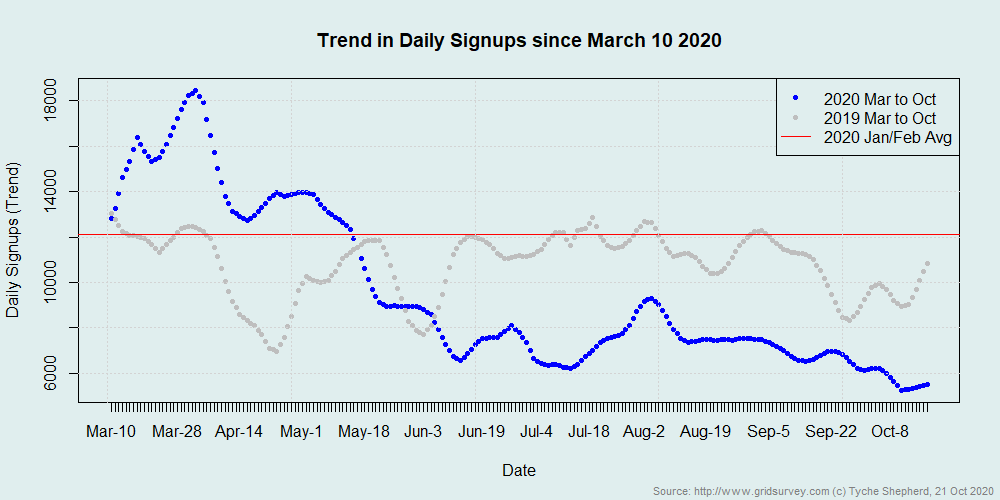

On the one hand, the second graphic included in her tweet appears to in part confirm commentary from the Lab itself: that 2020 has seen an upswing in the number of users returning to the platform, whilst also suggesting that – again, understandably, given the pandemic – that existing users were spending longer in-world in 2020 that had been the case in recent years. All of which is also to the good (particularly if returning users find reasons to maintain their engagement in the platform once more).

Second Life new user sign-ups 2020. Credit: Tyche Shepherd

However, on the other, the graphic reveals a niggling concern: whilst sign-up have remained relatively stable for a number of years, with occasional peaks and crevasses, 2020 saw a distinct decline in sign-ups from the end of March through until early October, despite an initial spike in sign-ups in the March-April period, again potentially fuelled by the pandemic. In particular, the drop-off not only saw sign-ups fall below the average set in the first two months of 2020, but also fall and remain below average sign-ups seen throughout 2019.

As such, Tyche’s figures tend to suggest that, while the Lab is determined to grow SL’s user base through the attraction of new users – a programme it has, to varying degrees, indicated it has been focused on since around mid-2019 – there is still a lot to be done in this area, if the hoped-for growth is to be realised. However, this is somewhat tempered by the fact that given the rise in median concurrency is in part fueled by returning users, it demonstrates that the Lab is correct in focusing a portion of its marketing efforts towards former users who have drifted away for one reason or another.

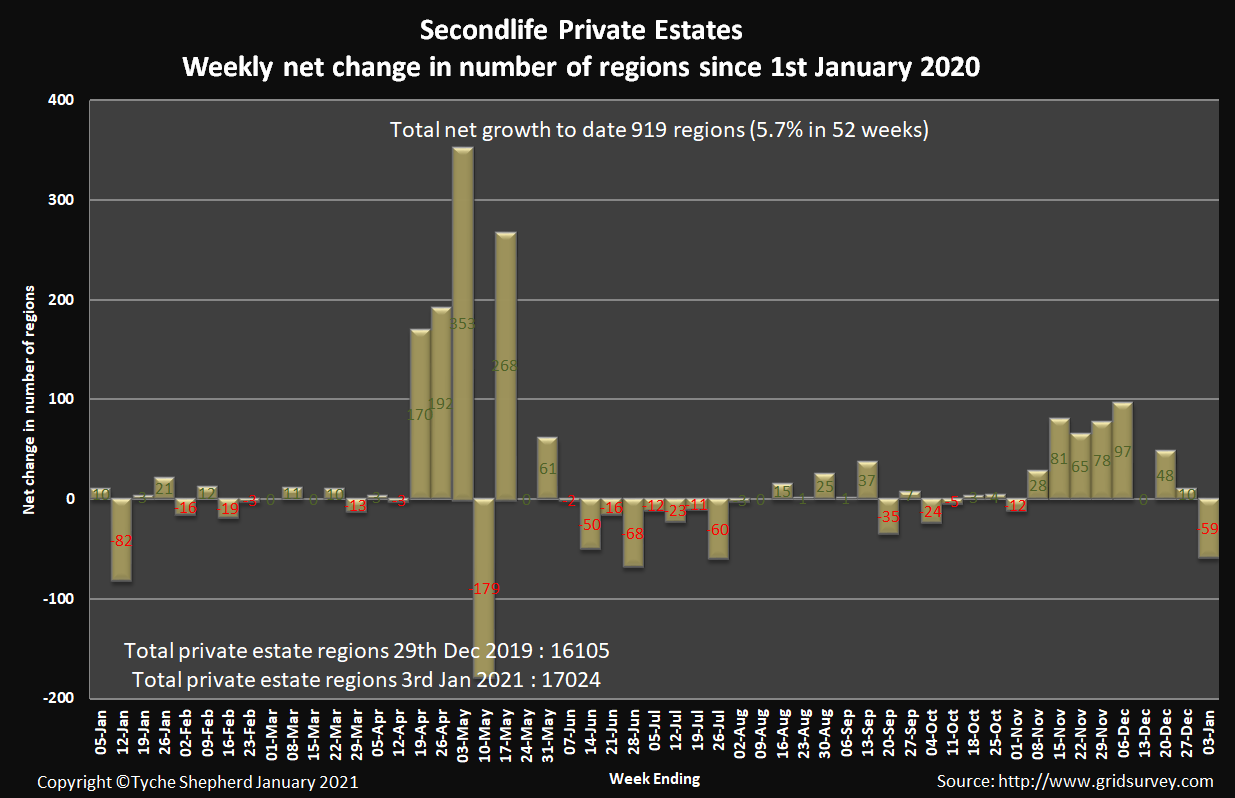

Land use – or more correctly, grid size – is another metric Tyche tracks, providing as she does regular reports on the overall size of the main grid and the comings and goings of both private and “Linden owned” regions. While the relative size of the grid, if looked at in and of itself only, can be a false or misleading indicator of the overall state of SL, tracking the number of private regions does help in building a picture of LL’s core revenue flow – region tier.

On January 3rd, 2021, Tyche tweeted her year-end analysis on private region numbers, revealing that 2020 saw an overall net growth of some 919 private regions (Full and Homestead) through the year, representing a 5.7% increase.

Second Life private regions in 2020. Credit: Tyche Shepherd

The majority of this growth came in two bursts: mid-April through to the end of May (with one significant period of shrinkage during the week to Sunday, May 10th, 2020), and then November-December 2020, immediately following the period of unavailability of new regions through the mid-months of the year resulting from the work transitioning SL to AWS services.

While the increase in the size of the grid is not exceptional when compared to increases seen prior to 2011/2012, it is still positive, indicating that there is a general willingness among users to invest in land, helping the Lab’s bottom line. The uptick in 2020 has meant that when the general reduction of Linden-held regions through the year is taken into account, the total number of regions in the grid grew by 3.3%.

Given the difficulties of 2020, Tyche’s figures tend to show Second Life held its own through what has been what might be termed a less-than-optimal year. With the Lab looking to further ramp-up advertising in 2021 (and perhaps further tweaking of the on-boarding process), it’ll be interesting to see how the overall level of users / size of the grid fares through the year.

The announcement of the fee change unsurprisingly caused some upset, with a couple of forum threads popping-up on the subject (see: MP fees raising to 10% per sale. Thoughts? and Second Life® is still a world of opportunities). Various points are raised in both threads, some fair, some perhaps not-so-fair. While I’m the first to note that I’m not in any way, shape or size a “merchant” or “commercial creator” in SL I thought I’d try to step back and try to take a broader look at fees and tier, etc., in general.

The first point to note is that in making the claim that the increase to the MP transaction fees still leaves them “significantly lower than most digital content commissions across the industry” while citing Apple and Google as examples, the Lab did so with a certain amount of spin.

The 30% charged by Apple, for example, incorporates payment clearing, fraud, indemnity, insurance, and dunning; local tax law enforcement & reporting; service provisioning and distribution, etc. Due to the nature of Second Life these fees are incurred separately to the MP – but they are still incurred by many merchants using the MP, and when taken into consideration, they amount to somewhat more than 10%, a point Cat Hunter makes in this comment.

Also in their blog post, the Lab note that that fee change is to help offset costs incurred at the Lab due to investing in new Marketplace features and improvements. This is fair enough; however, given that the first of these changes is apparently within weeks of being deployed (improved MP search filtering), it might have been an idea to perhaps to wait until these changes had been introduced before announcing the fee increase – and then to champion them alongside the improvements that have been made over the last 12-18 months, such as the much-requested Store Manager capability and the notifications and redelivery capabilities and wishlists and favourites¹.

However, there is a more intrinsic reason for fee increases – be they with transaction fees or anything else (such as the recent increases in Premium subscriptions), and it is one the Lab perhaps doesn’t communicate clearly: and that’s trying to reduce virtual land tier.

While tier has contributed to the loss of regions in SL, including places such as Venexia (above) and its sister region, Goatswood, lowering it without increasing fees elsewhere would always hurt Linden Lab more than help users

This is something that users have (rightly or wrongly – there are actually arguments on both sides of the coin) been demanding for at least the last decade. And since the start 2018, Linden Lab’s CEO, Ebbe Altberg, has repeatedly stated the company would like to reduce land tier – but would only be able to do so if the resultant loss of revenue the company would suffer as a result could be compensated for through other means².

In fact, the Lab have taken steps to reduce tier: in 2016 there was the private region buy-down offer³ (the interim boost to LL’s revenue as a result of the fees payable likely long since having passed), and in July 2018 reduced private region tier from US $295 to US $249 for Full regions (that now stand at US $229), and Homesteads from US $125 to US $1094.

While it is hard to accurately quantify, given the various factors involved (e.g number of grandfathered, skill and educational regions, the more recent slight increases in region count, etc.), it is – with the help of Tyche Shepherd’s Grid Survey and the Internet Wayback machine – possible to reasonably (conservatively?) estimate the impact of the July 2018 tier reductions at around a LS $300,000 a month fall in the Lab’s land revenue. This may not sound a lot – but it is something LL would likely want to recoup – and it can only be done through increases in other fees, as Altberg noted in his comments on the matter.

This should not be taken to mean the transaction fee is wholly associated with compensating for the tier reduction, but it’s not unreasonable to assume it might nevertheless help, either now or in the future. More to the point, and regardless of where the revenue from the MP fee increase is used, it wouldn’t hurt for the Lab to remind people of the strategy to pivot revenue away from land tier and to other options when making similar fee adjustments elsewhere (or indeed, the introduction of new fees, even it they may also help offset the cost of implementing new options and capabilities).

There are two final points that come to mind when looking at the MP transaction fee change. The first is that of all the fee changes thus far introduced, it is the one that merchants can most directly compensate for, as some in the forum threads have noted. Merchants can raise their MP prices, for example, whilst keeping their in-world prices lower (which is allowed5); or those with in-world stores might focus more on sales through that channel, with associated group advertising.

The second point comes back to the timing of the announcement. It would seem that the increase has been made so that the Lab can benefit from the likely increase in MP sales during the run-up, and indeed over, the holiday season. There’s nothing wrong with this per se; but given the increase has likely been on the cards for a while, it would have perhaps have been preferable had LL given more of a lead time on its implementation so allow merchants more time to prepare for it, and so help them in compensating in what might come across as a reduction in their own ability to generate revenue through the same holiday period.

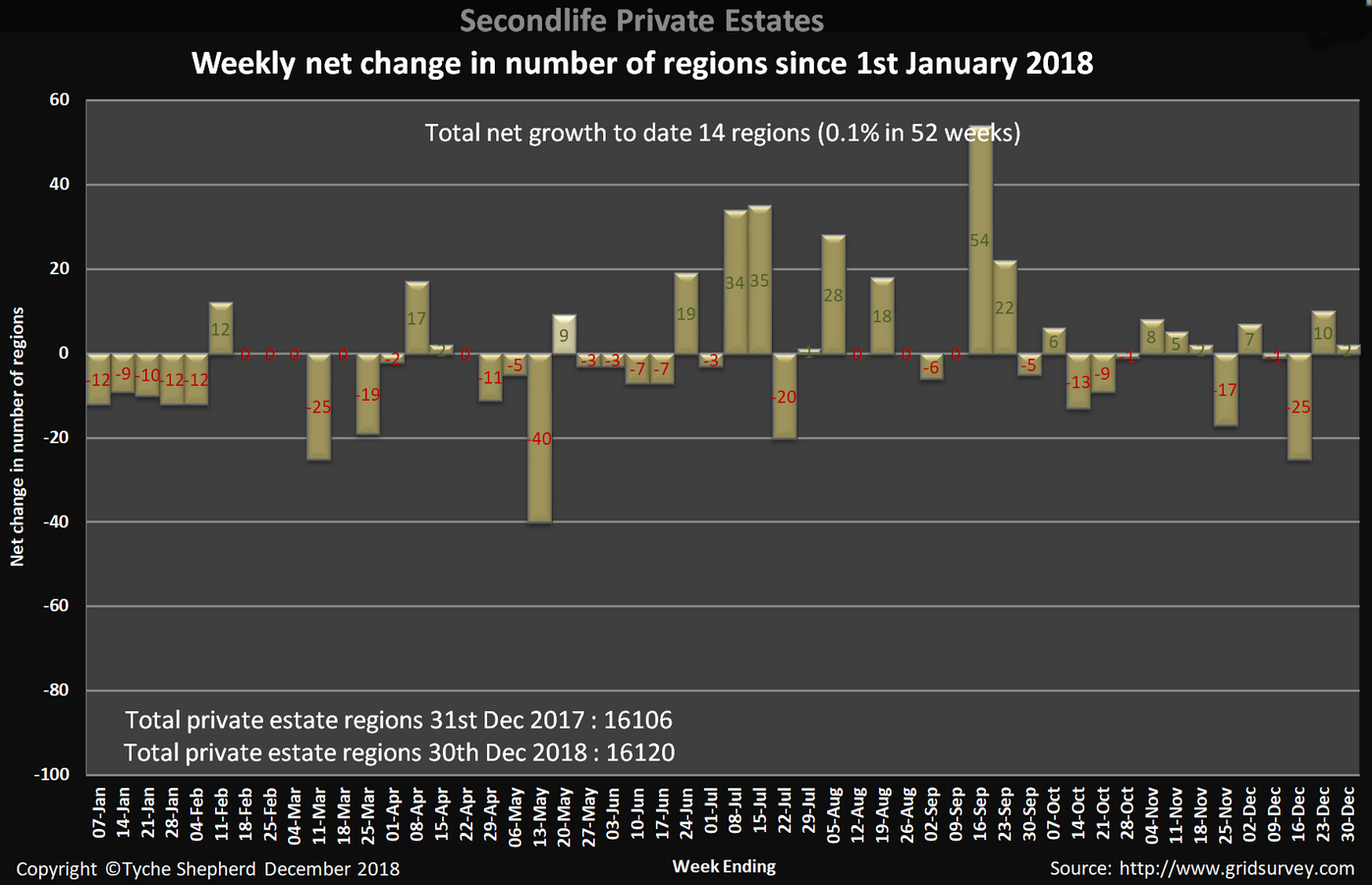

On December 30th, 2018, Tyche Shepherd tweeted a brief summary on the general size and state of the Second Life main grid.

The surface level reading in the summary is good: overall, the grid increased in size by 2.1% – the first such increase since 2011, leaving the grid at a total of 23,811 regions at the end of December 2018, compared to 23,337 at the end of 2017. However, where private regions are concerned – still the major revenue earner for the Lab – things were far more modest: just 14 regions up on the year, from 16,106 to 16,120 – a 0.1% growth. The rest came from Mainland, up 460 regions to 7691, thanks largely to the arrival of the SSP continent.

Taking the year-on-year figures for private regions from 2010 onwards (that being the previous year in which the grid exhibited a growth in the number of private regions), we get the following breakdown:

2010

2011

2012

2013

2014

24,483

23,857

20,994

19,273

18,600

Increase

%age

Loss

%age

Loss

%age

Loss

%age

Loss

%age

810

3%

626

2.56%

2863

12%

1719

8.2%

673

3.5%

2015

2016

2017

2018

17,775

16,783

16,106

16,120

Loss

%age

Loss

%age

Loss

%age

Increase

%age

825

4.4%

992

5.6%

677

4.0%

14

0.1%

Working on the basis of Tyche’s Full Private Region surveys I have to hand, a breakdown of approximate recent monthly revenues from private regions over the most recent five-year period might be given as:

November 2013: US $3,857,000 (+/- US $52,000)

March 2016: down to US $3,385,000 ( +/- US $43,000)

December 2016: down to US $3,162,000 (+/- US $39,000)

December 2017: down to US$ 2,970,000 (+/- US $36,500)

December 2018: approximately US$ 2,970,000 (+/- US $36,500)

Note the December 2018 monthly tier level reflects a growth of just 14 regions (most likely mixed between Full and Homestead), having minimal overall impact based on the margin of error.

The increase in private region is likely – as Tyche points out – due to the Lab’s downward adjustment in private region fees, announced in June 2018, and which came into effect as from the start of July 2018. Certainly, this was followed by an upswing in demand totalling 69 private regions over two weeks, although it might be argued that overall, the fee changes can’t yet be judged to have moved the grid into a sustained level of growth.

Private estate numbers downs and ups in 2018 – click for full size

In fairness, the reduction in costs for private regions wasn’t going to result in a massive upswing in demand. For one thing, the 15% reduction in monthly tier for a Full region – as I noted at the time – wouldn’t see people stampeding to get a region of their own. Thus, outside of events, etc., demand for land still largely lays with those in the land rental business, particularly given Homestead availability remains tied to having at least one Full region, and how well they are perceived as passing on the lower fees through reduced rental charges to customers, which itself could be complicated. Although all that said, it might have been hoped things came out a little stronger by year-end than has been the case.

So, what might we see in 2019 in terms of land?

Well, it’s unlikely Linden Lab will move towards another reduction so soon after that of July 2018, simply because more time will be required to analyse the overall outcome in terms of overall outcome. However, there are other things that will be forthcoming in 2019.

As noted, the largest growth in regions is the SSP continent (384 + a testing region). It’s no secret this is likely the new Linden Homes continent, due to come on stream in 2019. What is still to be seen is how they will be offered, how they might help generate revenue, and what effect they might have on the grid. For example, will they replace the existing Linden Homes entirely and be offered within the current Premium subscription package and ultimately intended to replace the existing Linden Homes continents? Will they form part of a new Premium subscription offering, sitting alongside the existing Linden Homes continents? If they are to completely replace the existing Linden Homes over time, what might be the logistics for doing so and for “retiring” the existing LH continents? Might we see more than one new Linden Homes continent deployed in the coming year?

2019 may well also see a large part of the Lab’s work in transitioning Second Life to the cloud. Even if this is completed by the end of the year (which is probably optimistic given the massive complexity of SL, but we’ll see), it’s also unlikely to lead directly to any adjustments to land fees or the release of new products, simply because, again as the Lab has indicated, they’ll need time to bed things in and ensure everything is running as anticipated and – equally importantly – experiment to see what (if any) kind of product options might be available and how they might be priced.

For my part, I suspect the sine wave we’ve seen in the second half of 2018 will likely continue, undulating between losses and gains, with a possible bias towards the positive side of the line. But that said, I didn’t foresee a fee cut for private regions coming in 2019, and actually expected numbers for the year to decline (albeit far more slowly than previous years); so what do I know? 🙂 .

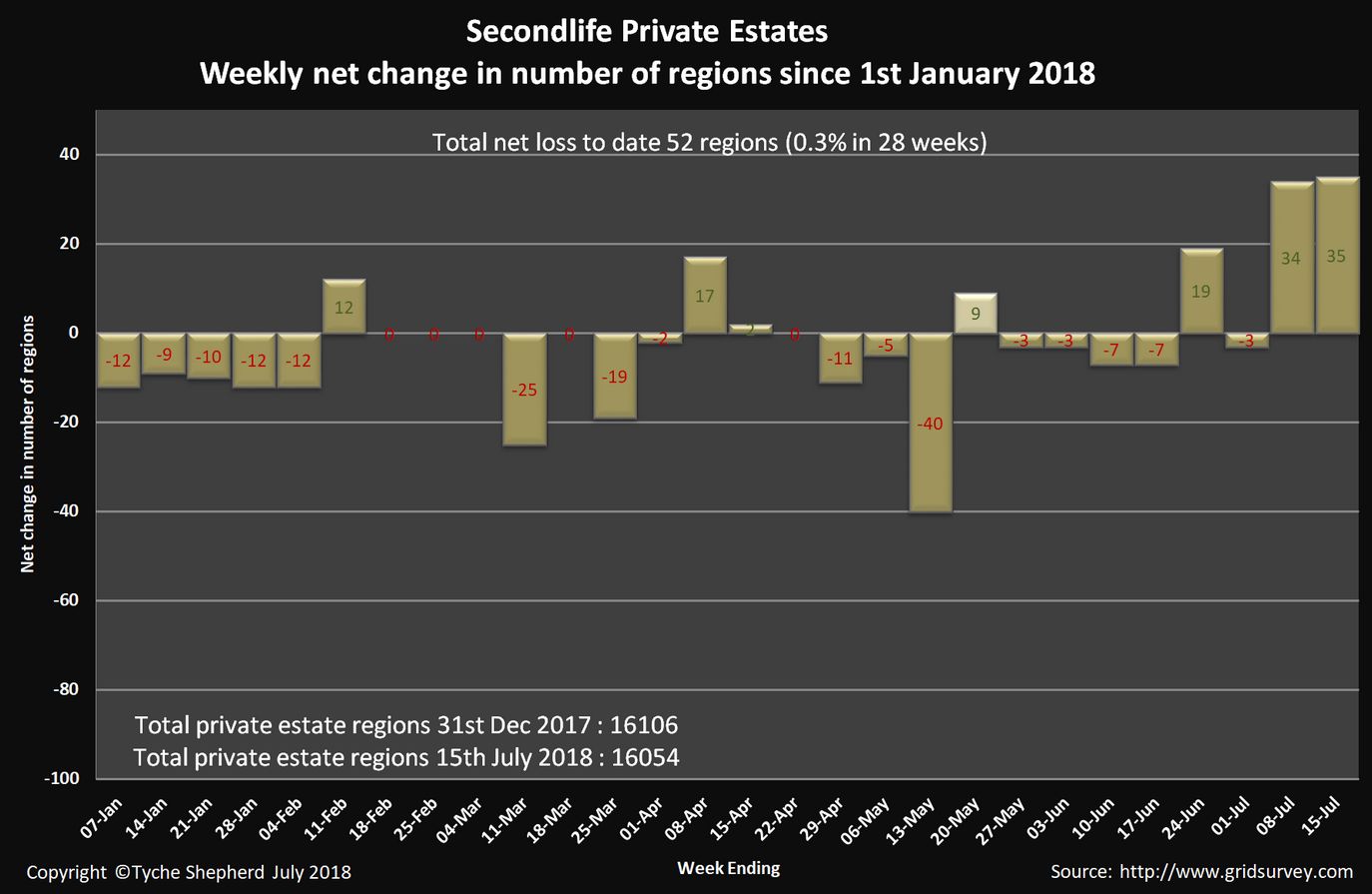

It’s been two weeks since Linden Lab introduced the new pricing structure for private regions, and as Tyche Shepherd reports, her Grid Survey shows the grid has experienced its second consecutive week of net private region growth since the change came into effect.

In the week immediately following the introduction of the new pricing structure (Monday July 2nd through Sunday July 8th), the SL grid saw a net increase of 34 private regions, while in the week Monday July 9th through Sunday July 15th, the net increase was 35 private regions.

As Tyche indicates, these increases have helped slow the overall rate of private region attrition to just 0.3% – a net loss of 52 private regions between January 1st, 2018 and July 15th, 2018. By comparison, some 326 private regions were lost to the grid between January 1st and July 16th, 2017 (with an overall net loss of 667 private regions through the entire year).

The two weeks following the private reduction pricing changes have seen net increases in the number of regions on the grid. However, it’s still too early to call this a trend or draw significant conclusions. Credit: Tyche Shepherd

So, have regions losses turned a corner as a result of the price change?

Frankly, it is too soon to tell; two weeks is only two weeks – we need to see how things trend out over a longer period before anything can really be determined. A lot here will depend on how much of the tier reduction land rental businesses pass on to their tenants in order to make private rentals more appealing; something I noted in passing in Looking at the new private region and L$ fees. Plus, a simple count of region growth isn’t the entire story here.

Simply put, the private region pricing restructure will have seen the Lab take a reduction in monthly revenue generation. It’s questionable whether such a modest increase in region numbers, even when coupled with other options for increased revenue generation such as the Mainland price restructuring (with its possible attendant increase in Premium subscriptions) and the US $0.50 increase on L$ purchase transaction fees, has wholly overcome the immediate deficit of the tier rate cut.

Thus, while the uptick in private region count is a positive turn, it is too early to be celebrating. We’ll need another 4-6 weeks before we can start to get a genuine feel for how things are going as a whole. It will also be interesting to see how long new regions entering the grid remain in place or whether we see some rapid comings / goings month-to-month. I’m also curious as to how the restructuring affects the Full / Homestead product ratio on the grid, so will be looking to see if Tyche can provide some updates on this in the coming weeks / months.

In the meantime – and totally off-topic as far as private regions are concerned – I wonder if Tyche has had time to have a bop around Mainland to see how the abandoned land situation there is fairing? As of January 2018, abandoned land stood between 22% and 23% of all Mainland; it would be interesting to see how it now stands, some four months on from the Mainland price restructuring.

A major goal at the Lab is to “re-balance” the Second Life economy – shifting the onus of their revenue generation away from a heavy reliance on virtual land leasing to distribute it more broadly across all fronts – land, Premium subscriptions, transaction fees, Marketplace fees, etc. Over the last few years we’ve seen some of this in action:

In April 2016, increases were made to all transaction processing fees and Linden Dollar processing fees (raising the latter by 30% to US $0.40 per L$ purchase).

In June 2017 increases were made to the maximum fee for processing credit transactions was raised to US $25, and the fee charged per L$ purchase was raised to US $0.60.

In November 2017, increases were made to L$ purchase fees (to US $0.99 per transaction) and to fees charged for transferring money via PayPal or Skill from the start of 2018, raising both to 2.5% with no maximum limit on the application of the fee.

Some of these increases were couched as being in part to meet the costs involved in the Lab handling the transactions and ensuring all proper fiscal and legal requirements for money handling are properly met. Doubtless, this was the case – the Lab has invested heavily in matters of compliance. However, it’s also not unfair to say that once the initial expense in performing this work has been recouped, these fee increases enable the Lab to both cover the cost of transaction handling and generate some revenue through such transactions (however modest on the individual transaction it might be).

On the other side of the scale, we’ve seen efforts to make virtual land more attractive – notably through the region buy-down offer of April-September 2016, and more recently the changes to Mainland pricing.

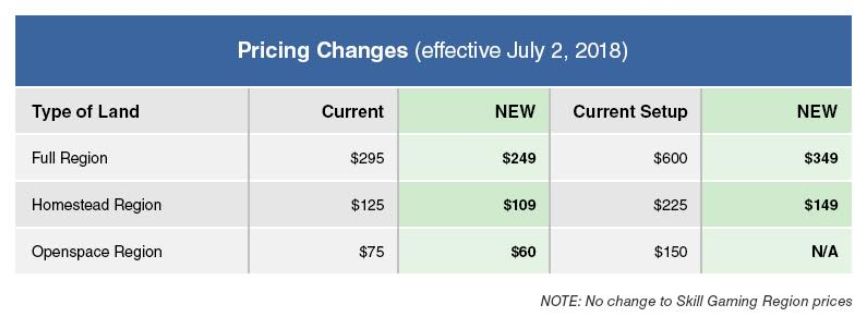

On July 2nd, 2018, the most ambitious change to private region pricing in Second Life came into effect: a reduction of 15% in private region maintenance fees (tier) for all current region types and reductions in the set-up fees for Full and Homestead regions (new OpenSpace (“water”) regions no longer being offered as a product from July 2nd, 2018).

These changes – it should be noted – come with a further increase in Linden Dollar purchase fees, which increase to US $1.49 per transaction.

New Private region pricing structure. Note that as from July 2nd, 2018, new OpenSpace regions will no longer be available as a product, and Linden Dollar purchase fees increase to US $1.49 per transaction

It’s fair to say that any change of this kind, be it in land pricing or transaction fees, can generate heated feedback (witness this forum thread on the 2017 increases). The changes to private region fees have been no exception, with views being expressed via in-world groups, within assorted forums (such as SLU) and even in blog comments. Some have been upset over the L$ transaction fee increase; others – notably those in the virtual land rental business – have been upset by the change no extending to grandfathered regions; others apparently don’t see the move as “enough”, protesting that the tier rate should be cut to US $195 (or similar). And there has been a fair amount of reaction to the L$ purchase fee increase.

Obviously, time will reveal the outcome of these changes, but as is my want, I’d pass comment on a few things.

When it comes to the land rental business, it is hard to see why the exclusion of grandfathered regions is being taken so negatively. For one thing, these are already below the new tier rates, as the Lab states. Further, it is now 18 months since the buy-down offer closed. This should have been enough time to recover the up-front cost of converting regions to grandfathered status (US $600 / Full; US $180 / Homestead), and now leave rental companies in a position to enjoy a modest increase in income from such regions whilst also offering customers using them a degree of lower rent.

Which is pretty much also the opportunity they have with this tier reduction. Frankly, 15% is unlikely to have people leaping in droves to buy Full regions directly from the Lab. But what it might do is once again increase people’s desire to have Homestead regions as private homes. Given that these remain tied to holding at least one Full region, it’s not unfair to say that should it happen, land rental companies can only benefit. And even if the private land market remains relatively flat, such businesses should still be able to lower their rental rates to attract new customers without damaging their existing margins.

So it really is hard to see why some in the land rental business are so put out by grandfathered regions being excluded, or to claim they get “none” of the benefits of this fee reduction.

When it comes to the increase in Linden Dollar transaction fees (which with this increase will have rise by 198.4% since April 2016), the impact will perhaps be harder to gauge, simply because people can offset at least some of the impact by adjusting the amounts of Linden Dollars they purchase in a single pass. Just how much of an offset can be achieved depends on a range of factors – the amount of L$ someone buys in a single pass, how easily they might be able to consolidate purchases, etc. – but this doesn’t deny the fact it is precisely what people have been doing as a result of past increases.

Even so, it will in interesting to see what, if any, impact this has on actual spending in SL – although I suspect that changes to fees elsewhere that have been hinted at (such as with the Marketplace) might have more of a visible impact, if and when they come into effect.

There will always be positives and negatives to just about anything the Lab does. However, “the tier is too damned high!” has long been a mantra within Second Life and while it is “only” a 15% reduction in tier, this is a positive step towards addressing this mantra when it comes to private regions fees (and it’s not unreasonable to assume there might yet be more in the future – although they are unlikely to be even close to appearing over the horizon at this point in time). Similarly, while people are likely to continue to be put out by it, the increase in to the L$ transaction fee is a relatively “fair” move, as it spreads at least some of the burden of revenue generation for the Lab across a much broader section of the SL user base.