I haven’t written too much about “consumer” virtual reality and / or augmented reality during 2018, primarily because this past year has been rather quiescent when compared to 2017 and earlier, so outside of one or two events, there hasn’t been that much I’ve been prompted to write about. As such, and as we pass from 2018 to 2019, it seems a good time to take a broad look at both and where they might be going, at least from a purely armchair perspective.

In doing so, I’m not attempting to set myself up as any kind of “expert” or offer predictions per se; I’ve simply been gorging myself on a wide range of articles and reports on AR, VR and mixed reality over the last few weeks to catch up on everything, and with this article I’ll focus on virtual reality.

(Note that in writing this article, I’m deliberately ignoring two products that involve VR: Microsoft Mixed Reality and Apple’s rumoured AR / VR system. The former, because Microsoft appears to be playing a much longer game, and it is unclear how MMR will impact markets down the road; the latter because it’s unclear how Apple’s product will mix AR and VR, it’s overall capabilities, price point or precise nature.)

Consumer focused virtual reality has always had a hard mountain to climb. From the start, predictions of its growth verged on the ridiculous. At the end of 2015, for example, TrendForce claimed sales of VR hardware, software and services would hit US $70 billion by 2020, a figure that, at the time tended to be taken for granted despite the fact that when it was made, the consumer versions of the Oculus Rift and HTC Vive hadn’t even started shipping. Nor were TrendForce alone in the hyping.

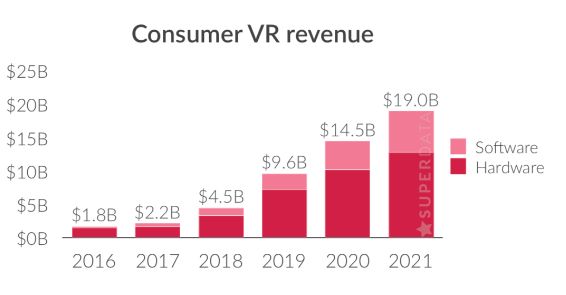

Obviously, VR hasn’t achieved anything like this kind of volume, but it is growing. In 2017, for example, total VR hardware and software sales reached US $2.8 billion, three years ahead of the time frame IHS Markit (one of the more reserved analytics companies looking at VR in late 2015) predicted. In 2018, this increased to US $3.3 billion; a relatively modest growth, but not unexpected given that outside of the Oculus Go, there haven’t been any major releases of VR headsets. This modest growth in sales, coupled with the lack of exciting new hardware releases has perhaps lead to more negativity around VR being voiced than previous years. However, 2019 could be the start of a “turnaround” for VR.

As it is, SuperData, which specialises in analysing the computer and gaming sectors, predicts that the VR market will double total revenues to US $9.6 billion in 2019. They further suggest revenues could grow to US $19.0 billion by the end of 2021. These might again sound like inflated figures – particularly the idea of a five-fold revenue increase in just three years, but there are actually two or three reasons to suggest why 2019 could well see significant growth in revenue for VR, and which will see it continue to trend upwards at a rate somewhat faster than seen thus far.

Up until the arrival of the Oculus Go earlier in 2018, consumer VR hardware had been more-or-less split into three areas: high-end tethered systems requiring upmarket PCs to power them; units dependent on the use of smartphones for a more limited immersive experience, and what might be termed a purely games oriented solution in the Sony Playstation VR. As such, all have been somewhat limited in their appeal / reach.

However, in 2018 the Oculus Go arrived, and in 2019 it is set to be joined by the Oculus Quest and the Vive Focus. The significance of these three units is that they are entirely self-contained and provide an immediate VR experience right out-of-the-box. No need to hook up a heavyweight PC (possibly at added expense) for the heavy-lifting, or to have a suitable smartphone to provide the visuals.

While both the Quest (shipping in 2019) and the Focus (currently only available in China) have yet to become globally available, their potential impact might be seen in the positive response the Go generated at launch, as noted by SuperData:

Oculus Go is part of an important movement. Facebook sold more units of the standalone headset in its launch quarter than they did the Oculus Rift in the entire first half of 2017. Its price and convenience are proving to be selling points.

– Stephanie Llamas, SuperData Head of XR data research

What is particularly interesting about the response is that it has not been limited to purely “home” use. While the Go is marketed as an “entertainment” headset, it has already been seen as a means of expanding VR’s use within enterprise markets. Take Walmart as an example.

One of a number of major US corporations to have invested in VR (a list that includes Boeing, Tyson Foods, UPS, and Ford), Walmart has been using the technology to get staff quickly up-to-speed with new technologies, and to improve their customer service, care and compliance techniques. It’s an approach that has proven popular with staff, but the cost of tethered VR (headsets and supporting PCs), limited the company to only deploying VR to their regional training centres.

Life happens in 360, not 2D video. We test our associates on the content they see. Those associates who [used] VR as part of their training scored higher than those who didn’t. We had associates standing in line to get trained. That never normally happens. So we knew we had something.

– Brock McKeel, Walmart Senior Director of Digital Operations

However, the release of the Go and its low price point encouraged Walmart to procure 17,000 of the headsets and start deploying them across 4,600 stores in the United States, allowing them to bring immersive training directly to their staff in volume.

Over time, Walmart and unlikely to be alone in taking such an approach. Take education as another example. SuperData believe demand for VR is potentially as high as 46% amongst educators of all backgrounds polled. However, the average cost of a tethered Rift or Vive headset coupled with the cost of an associated PC (approx US $1,500 per unit), makes equipping a 30-desk classroom prohibitively expensive. However, the US $199 32GB Go brings the cost down to US $6,000 – far more in keeping with budgets.

It’s not all plain sailing, however. As an off-the-shelf product, the Go lacks enterprise-level control: specific features and controls (such as access to application installation or dropping to the Oculus Home experience) cannot, by default, be locked. Thus its appeal as something like a teaching tool might be seen as limited. Walmart have got around this by working with Strivr, a company specialising in providing training experiences with the kind of enterprise-level tools required to manage training and study.

Given their greater price point (US $400 and US $600 respectively), the Quest and Focus may not find a footing within education, but they could nevertheless see application in other markets just as the Go has. Given that both SuperData and ABI Research see enterprise markets as significant contributors to VR’s growing revenue (ABI project that enterprise use of VR could account for almost 50% of VR revenue by 2021 – some US $6.6 billion), both the Quest and the Focus could have a an important role to play in kick-starting this growth.

The significance with enterprise use of VR using standalone units like the Go, Quest and Focus, is that it can help VR gain far broader acceptance, with people being more willing to bring it into their homes. This is because a) they have experienced it within their workplace; b) the hardware involved is (more-or-less) the “same” as the hardware they are buying (familiarly encourages both trust and experimentation) and c) the price factor.

Even without the enterprise element, the Go, Quest and Focus could prove influential in greater take-up of VR in the home, because (again) the price point (in the case of the Go) makes purchase relatively “risk free”. While the Quest is US $250-ish more than the 64 GB Go, it could still be seen as attractive enough to be seen as a reasonable proposition.

Previous iterations of our report have tracked the market as it has gained momentum, and we believe the launch of Oculus Quest will be a major force in pushing it over the tipping point into the mainstream.

– Stephanie Llamas, SuperData Head of XR data research

From my own perspective, I still don’t believe VR will become as all-pervasive as some believe; nor do I believe there is some mysterious, yet-to-be-discovered “killer app” waiting to be found that will cause billions of people to want to grab headsets and dive into VR.

Rather, I do remain of a mind that VR will, in the coming years, find its niches across a range of markets, and thrive as a stable and useful – if not disruptive – technology. As such, I would suggest that much of the negative press and commentary around VR we’ve recently seen in some sectors of the press will prove to be as incorrect as all the early talk about the massive growth in VR that would occur between 2015 and today.

I’m also still of the opinion that when it comes to reach and acceptance, augmented reality (together with mixed or extended reality) that will prove to be the more genuinely disruptive technology and have the greatest impact on our daily lives. But I’ll save looking at that for the next part in this series.

I believe Microsoft’s ‘Vision’ for #MR will prevail in the long run. The ‘Killer #VR/#AR Apps’ are already here (Simulation, Training, Data Virtualization, #MRPresence). The Industry just needs a better Sales, Marketing & Support Channel. ps. Have you tried SL using @VRDesktop yet? If not, you should!

LikeLike

I do agree that MR (or XR, as Qualcomm like to call it) will be the way forward, hence mentioning in passing that MS are playing a longer game with their MR systems, and will have more to say on this in the follow-up article(s).

I actually don’t believe in the “killer app” philosophy, as it implies a single, all-encompassing “need”. Rather, as I’ve stated and you note – VR has a range of applications (and I’d add prototyping, design, architecture to your list as well as healthcare), and AR’s are potentially far, far, broader and more naturally lifestyle and business complimentary. However, were I to put a finger on VR’s most obvious route to a mass market in terms of a “killer app”, I’d actually say that “killer app” will actually be the rise of AR, together with the merging of VR / AR into MR / XR. That’s something I’ll be explaining (if it needs explaining 🙂 ) in the next article in this series.

I’ve not tried SL in VR Desktop, simply because I don’t have a headset of my own (I have to rely on occasionally borrowing a Rift from a family friend). I’ve also no intention of getting one at present, as I want to see how the technology matures, headset-wise. Again, my interest is perhaps far more directed towards AR / MR / XR.

LikeLike