Last week an article appeared in New World Notes (NWN) which seemed intent on giving the impression that Second Life is in a state of terminal decline. The headline proclaimed: “Second Life Has Lost Over 650 Sims & $1 Million in Yearly Revenue in 2011; This is Why SL Can’t Survive as a Niche”, followed by a comment that, “The only future for Second Life is several millions of users, or none at all”.

Provocative reading perhaps; but how reasonable is it to make such assertions?

Provocative reading perhaps; but how reasonable is it to make such assertions?

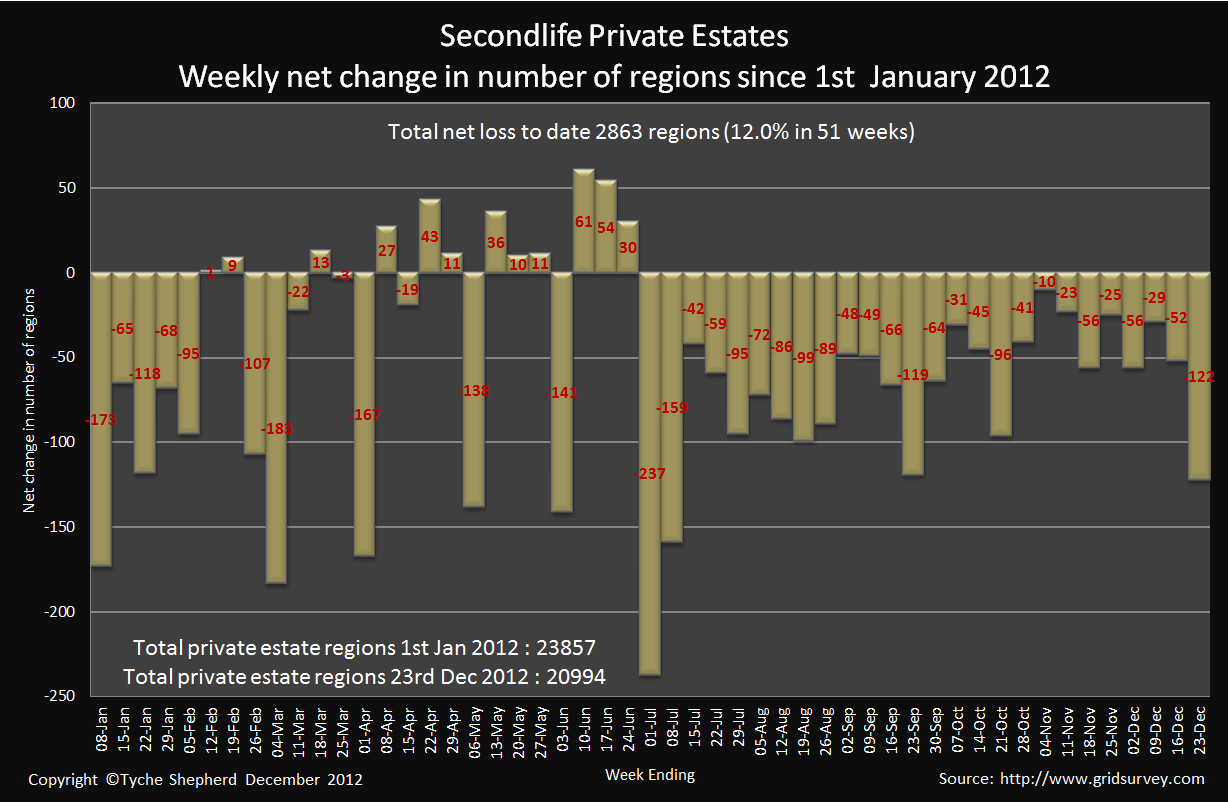

Well, first and foremost, I don’t dispute the figures in terms of region losses or potential revenue drop. They’ve been taken from Tyche Shepherd’s excellent Grid Surveys, which week-by-week look at the overall status of the grid in terms of regions, private and mainland. Rather, I tend to find the conclusions the author draws from Tyche’s figures to be somewhat questionable.

The Ebb and Flow of the Statistical Tide

Let’s try to put things in a little perspective, starting with two points in particular:

- 650 regions is around 2.6% of the total land mass

- Linden Lab has an inward flow of revenue of some $75 million a year. As such, $1 million amounts to a 1.3% drop in that revenue. All things considered (economic climate, etc.), that’s not an horrendous drop.

Now let’s take a look back at private regions in SL over the last three years (a not unreasonable time-frame in business terms).

- 2009:

- Jan-May SL suffered a loss of 1095 private estates during the first 5 months (from 22406 to 21311); no doubt fuelled in part by the OpenSpace fiasco

- June-December: SL grew to 24033 private estates, an increase of 1627 regions over the start-of-year

- In 2010:

- SL grew by 6% overall in terms of regions

- 44% of this growth lay in private regions, representing an overall growth of 3% for private regions

- In 2011:

- Jan-Aug: 2.6% loss of private estates

- A potential 3.9% loss by year-end.

In other words, in 2009, private regions on the Grid grew by some 7.26% over the start-of-year figure, despite an initial loss of some 4.88%. In 2010 it grew by a further 3% in private regions.

So while a current 2.6% drop is cause for some concern – it’s not yet drastic. Even if the shrinkage continues through to the year-end (as seems likely, given Tyche’s latest figures), and yields a potential 3.9% drop in private regions, the situation still would not be terminal.

Recession does Nasty Things

There is another factor to consider here. Right now, we’re in the midst of a prolonged global economic downturn. The longer it goes on, the deeper it bites into people’s disposable income. A prudent observer of the current decline in private regions in SL would consider it possible – likely, even – that the recession is responsible for at least some of the shrinkage we are currently seeing. One sees little sign of this in the NWN article.

But downturns don’t last forever (or if this one does, we’ll all have a lot more to worry about than Second Life). Therefore (and while past performance may not always be indicative of future growth), it is no unreasonable to suggest that once the economy does start to improve, people will again have more disposable income they can put towards Second Life, and this is likely to result in an improved demand for land as a result and at least slow – if not reverse – the current trend in private region losses.

Alternatives

Nor do Linden Lab need to convert anywhere near 400,000 users to Premium membership in order to recoup falling land tier income (even should this be necessary), as the NWN article also dramatically suggests.

Right now, Linden Lab generates some 20% of its income – $15 million – through non-land related activities. As such, it only needs to increase that $15 million revenue by some 10% to help offset the losses experienced to date – a not impossible figure.

There have already been a couple of small moves in this direction; we’ve seen the introduction of upload fees charged for mesh imports and a push to generate more Premium memberships. While the former might not have a significant impact in the scheme of things, the same is not necessarily true of the latter. Were Linden Lab to offer a Premium membership package that gave clear and significant benefits to those already engaged in Second Life (rather than just new users, as seems to be the case with the current offering), then the potential uptake could be significant – and relatively rapid.

Beyond this is the fact that Linden Lab doesn’t necessarily have to look at Second Life to recoup “lost” revenue. The company is shortly to launch new products into the marketplace. While details have yet to be released, it is unlikely Linden Lab will do so without the means to leverage them into revenue.

True, the results may not be immediate (depending on how these new products are to be monetized and how they are received by the world at large). However, that the company is launching new products means that it will be less dependent solely on Second Life for revenue. An optimist might even speculate that as a result, Linden Lab might have a greater degree of freedom to better restructure / improve the Second Life platform.

Nor should these products be classified (/dismissed?) as some form of “SL Light”, again as New World Notes suggested.* To quote Rod Humble himself in reference to this idea: “I never said a lite version. I said and I mean new products which are in the area of shared creative spaces. or social creative tools or user-created virtual worlds/places if you prefer”.

Where is Everybody?

Truth be told, there is one figure that gives continued cause for concern for many within Second Life – and it is not region counts; it’s user concurrency. This has been in a steady state of decline for the last three years. In her end-of-year summary in 2010, Tyche Shepherd estimated that SL’s average concurrency levels equated to just 1.57 avatars per region. That’s an awful lot of empty space.

Now to be fair, the New World Notes article I refer to at the top of this piece does indicate that Linden Lab needs to do more to get people involved in Second Life – even if it does over-egg things by putting the figure in the “millions”. And keeping on the side of fairness, Linden Lab have themselves indicated that they are working on the means to get people directly involved in in-world activities (i.e. content creation, engaging in the economy as consumers, etc.) a lot sooner than is currently the case. However, one has to admit that it would be nice to see some practical outworking of these ideas before the year’s end. Even a gentle increase in user concurrency that can be sustained for more than a few months would be good news for just about everyone involved in SL.

Niche isn’t Bad

Finally, and in turning to the claim that SL cannot survive as a niche, one has to ask, “Why not?”. The fact is that Second Life has survived for some 10 years as niche product, and has managed to generate a tidy revenue stream for Linden Lab that has made them “Very profitable”, to use Rod Humble’s words, in the process. Get the flow of people into SL right and the mechanisms of engagement in place, and there is no reason why it cannot continue to do so and enjoy practical growth.

This is not to say that things won’t have to change in time; the reality is that Second Life and Linden Lab will be facing challenges in the coming years that may yet force significant changes to aspects of how things are run (such as, ironically, land tier). However, these needn’t necessarily be negative – although they will need to be planned for and carefully executed.

And what is so bad about being niche anyway? Many a company and product have enjoyed long and fiscally healthy times being precisely that.

—–

*Hamlet has pointed out that his article drew the distinction between any new products and SL; as such, I’ve amended this piece and apologise for any upset caused.

Tyche Shepherd has

Tyche Shepherd has